Key Takeaways

Nuclear startups innovate with small reactors, attracting $1.1B in funding by late 2025. Explore challenges in manufacturing & human capital for tech enthusiasts.

Overview

The nuclear industry is undergoing a significant renaissance, with substantial investor interest propelling nuclear startups into the spotlight. In late 2025, these innovative ventures successfully raised $1.1 billion, reflecting strong optimism in the potential of smaller, advanced reactor designs.

This surge in capital is critical for tech enthusiasts and innovators watching the energy sector, signaling a potential disruption to traditional power generation models. These startups aim to overcome the massive cost overruns and delays that plagued prior large-scale projects like Vogtle 3 and 4 in Georgia.

Traditional U.S. reactors like Vogtle 3 and 4 faced an 8-year delay and incurred over $20 billion in budget overruns, despite generating over 1 gigawatt each. The new approach focuses on modularity and mass production to drive down costs.

This article delves into the technological and manufacturing hurdles these promising startups face, exploring market context and future implications for the innovation ecosystem.

Key Data

| Reactor Category | Key Characteristics | Challenges/Advantages | Recent Impact/Status |

|---|---|---|---|

| Traditional Nuclear Reactors | Massive infrastructure; 1+ GW output; tens of thousands of tons concrete; 14 ft fuel assemblies. | Vogtle 3 & 4: 8 years late, >$20 billion over budget. | Historically dominant, but with significant project risks. |

| Small Modular Reactors (SMRs) (Startup Focus) | Shrinking reactor size; modularity for scalability; aim for mass production. | Potential for reduced costs and faster deployment via manufacturing learning. | Nuclear startups raised $1.1 billion (late 2025). |

Detailed Analysis

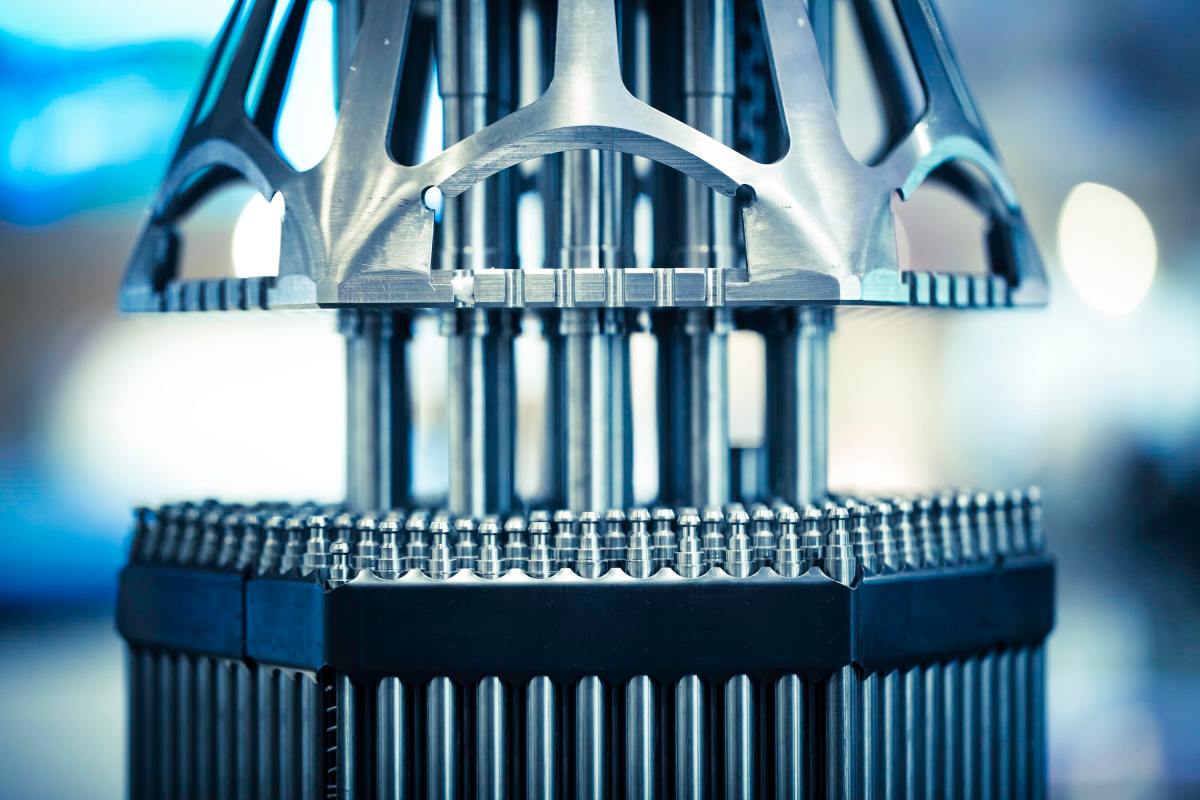

The global energy landscape is undergoing a profound transformation, positioning advanced nuclear technology, particularly through nuclear startups, as a critical component of future power grids. This burgeoning interest marks a significant pivot from the past, where the industry grappled with the sheer scale and complexity of traditional, gigawatt-plus reactors. The recent resurgence, fueled by substantial investor confidence, underlines a strategic shift towards innovation in design and deployment. Historically, projects like the Vogtle 3 and 4 reactors in the U.S. exemplify the monumental challenges inherent in this traditional model, experiencing delays of eight years and budget overruns exceeding $20 billion. This backdrop sets the stage for a new generation of reactor development, where agility and cost-efficiency, central to the startup ethos, are paramount. Innovators are now seeking to leverage smaller, more modular designs to circumvent the pitfalls of their colossal predecessors, aiming for a more resilient and scalable energy infrastructure.

The core premise driving these nuclear startups lies in the power of miniaturization and modularity. By shrinking reactor dimensions, they envision a future where reactors are not bespoke colossal structures but rather mass-produced units. This approach inherently promises a “learning curve” in manufacturing, where increased production volume leads to improved efficiency and, critically, reduced costs. This concept, while compelling, faces formidable execution challenges. Manufacturing, especially in highly regulated sectors like nuclear, demands deep expertise. Milo Werner, a General Partner at DCVC and a veteran of Tesla and FitBit’s manufacturing scale-ups, highlights the scarcity of essential materials in the U.S., forcing reliance on overseas supply chains. Her insights reveal a concerning erosion of domestic manufacturing “muscle memory” over decades of offshoring, impacting everything from factory construction to skilled operational staff, which poses a significant hurdle for these pioneering tech ventures in India and globally.

The manufacturing challenges for nuclear startups are not unique, mirroring struggles in high-tech hardware and even automotive sectors, like Tesla’s Model 3 scale-up. Yet, U.S. nuclear ventures face a diminished domestic manufacturing base, often sourcing crucial materials overseas. Milo Werner highlights that while these startups possess abundant capital, the critical human capital gap remains. Decades without significant U.S. industrial facility construction led to a profound loss of experienced manufacturing personnel, from floor staff to leadership. This “muscle memory” deficit is a shared challenge across American manufacturing, underscoring the need for sustained investment in skills and infrastructure far beyond initial funding. [Suggested Matrix Table: Comparison of Manufacturing Challenges: Capital vs. Human Capital for Nuclear Startups vs. Tech Manufacturing Startups]

For tech enthusiasts, innovators, and startup founders, the resurgence of nuclear startups offers a compelling case study in deep tech innovation. The immediate takeaway is that while significant capital is available, successful scaling hinges on overcoming foundational manufacturing and human capital deficits. Developers should recognize the urgent need for skilled talent in advanced manufacturing. Startup founders in this space must prioritize modularity, allowing for early production data collection and iterative improvement to build investor confidence. The long-term implications for India’s energy and tech sectors involve observing how these global supply chain and workforce challenges are addressed. Success here could redefine clean energy production, but it will demand sustained, decade-long commitments to re-establish industrial expertise and infrastructure. This era tests the resilience of innovation against practical industrial realities.