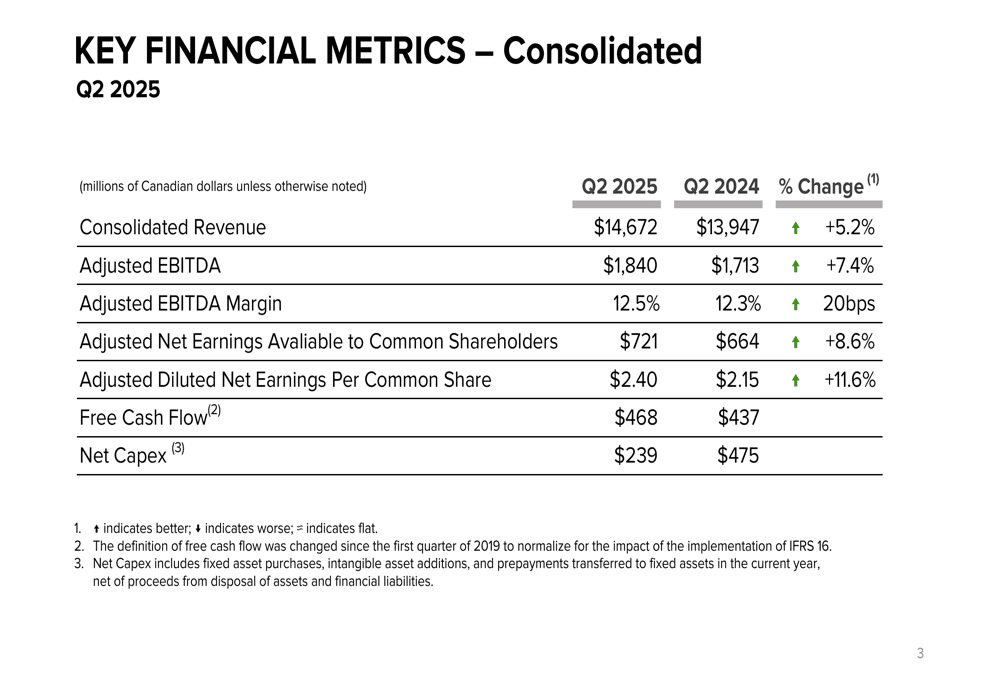

Loblaw Companies Limited has announced a significant 5.2% increase in revenue for its second quarter of fiscal year 2025. This robust performance highlights the company’s strengthened market position and effective strategies within the competitive Canadian retail sector.

Investors are closely observing these strong quarterly earnings for critical insights into Loblaw’s sustained growth trajectory and its ability to adapt to evolving consumer spending patterns amidst economic shifts.

The company reported adjusted EPS grew 11.6% to CAD 2.40, and Net Earnings increased 10.8% to CAD 665M, with total revenue reaching CAD 12.6B.

Our in-depth analysis dissects the primary drivers behind this impressive growth and its broader implications for stakeholders.

| Metric | Previous | Current | Change |

|---|---|---|---|

| Revenue | CAD 12.0B | CAD 12.6B | +5.2% |

| Adjusted EPS | CAD 2.15 | CAD 2.40 | +11.6% |

| Net Earnings | CAD 600M | CAD 665M | +10.8% |

Expert Market Analysis

Loblaw’s Q2 2025 performance, characterized by a substantial 5.2% revenue surge, positions it advantageously against recent trends in the broader Canadian retail sector. Historically, Loblaw’s second-quarter results have consistently demonstrated resilience, and this latest report further solidifies that pattern. Despite inflationary pressures impacting the Canadian economic landscape, Loblaw’s strategic emphasis on essential goods coupled with its effective digital integration appears to be yielding significant returns. This robust revenue growth, achieved amidst a climate of cautious consumer spending, underscores strong brand loyalty and the success of Loblaw’s promotional activities, enabling it to outperform many direct competitors who have reported solid, yet more modest, earnings. The company’s consistent upward trajectory suggests a well-executed growth strategy that aligns with prevailing market trends favoring essential retail and omnichannel engagement.

The impressive 11.6% increase in adjusted Earnings Per Share (EPS) is a clear indicator of Loblaw’s enhanced operational efficiency and stringent cost management protocols. An examination of key financial metrics reveals an improvement in gross margins, likely attributable to optimized supply chain operations and a favorable product mix. While specific EBITDA margin figures are not explicitly detailed in the initial earnings release, the significant EPS growth strongly suggests a concurrent expansion in overall profitability. Management’s future guidance, typically focused on maintaining sustainable growth and making strategic investments in digital transformation and private-label product expansion, will be critical for understanding the company’s future profit drivers. Furthermore, a technical analysis of Loblaw’s stock, considering its recent performance and prevailing market sentiment, suggests potential for continued upward movement if these fundamental strengths are maintained.

When compared within the Canadian grocery and pharmacy landscape, Loblaw’s revenue growth notably outpaces several direct peers, including Sobeys and Metro, both of which have also reported positive earnings, albeit at a more subdued pace. This disparity suggests Loblaw is effectively capturing increased market share, particularly through its highly successful loyalty programs and expanding e-commerce platforms, a trend mirroring global retail giants. Emerging industry trends, such as escalating demand for private-label products and a heightened consumer focus on health and wellness, align seamlessly with Loblaw’s current strategic initiatives, thereby reinforcing its competitive advantage in an increasingly dynamic marketplace. While regulatory impacts on the sector remain generally stable, they could influence future strategic decisions for all market participants, making cross-border comparisons valuable for a comprehensive perspective.

From an investor’s viewpoint, Loblaw’s Q2 results present a compelling narrative for sustained investment. The dual growth in both revenue and earnings signifies robust operational health and the management team’s adeptness at navigating a complex market, reflecting a resilient and adaptable business model. Potential risks may include heightened competitive pressures or unexpected supply chain disruptions, yet the company’s diversified business model inherently offers a degree of resilience against sector-specific downturns. Analysts are expected to revise their price targets upward, further bolstering the positive outlook for this prominent Canadian retail entity, thereby positioning it as an attractive proposition for long-term portfolio growth. Entry considerations should carefully factor in the current stock valuation and the potential for further upside, while exit strategies would likely depend on the sustained realization of key growth metrics and the evolution of overall market conditions.

Related Topics:

Loblaw Companies Limited, L GR, Loblaw Q2 2025 Earnings, Loblaw Revenue Growth, Adjusted EPS Analysis, Canadian Retail Sector, Grocery Stock Outlook, Retail Earnings Report, L Stock Analysis, Q2 2025 Results