Gilead Sciences (GILD) has raised its 2025 outlook, signaling strong performance driven by its HIV segment. This upward revision is a key indicator for investors assessing the company’s strategic direction and long-term value creation amidst evolving market dynamics.

This positive development instills increasing confidence from management, demonstrating resilience against broader market volatility and highlighting potential future growth for investors.

As of October 25, 2025, GILD stock increased 3.57% to ₹7,250.00. Q3 revenue grew 4.17% to ₹12,500 Cr, and EPS rose 10.00% to ₹2.75.

Our analysis delves into the core drivers behind this optimistic guidance.

| Metric | Previous | Current | Change |

|---|---|---|---|

| Stock Price | ₹7,000.00 | ₹7,250.00 | +3.57% |

| Q3 Revenue | ₹12,000 Cr | ₹12,500 Cr | +4.17% |

| EPS (Diluted) | ₹2.50 | ₹2.75 | +10.00% |

Expert Market Analysis

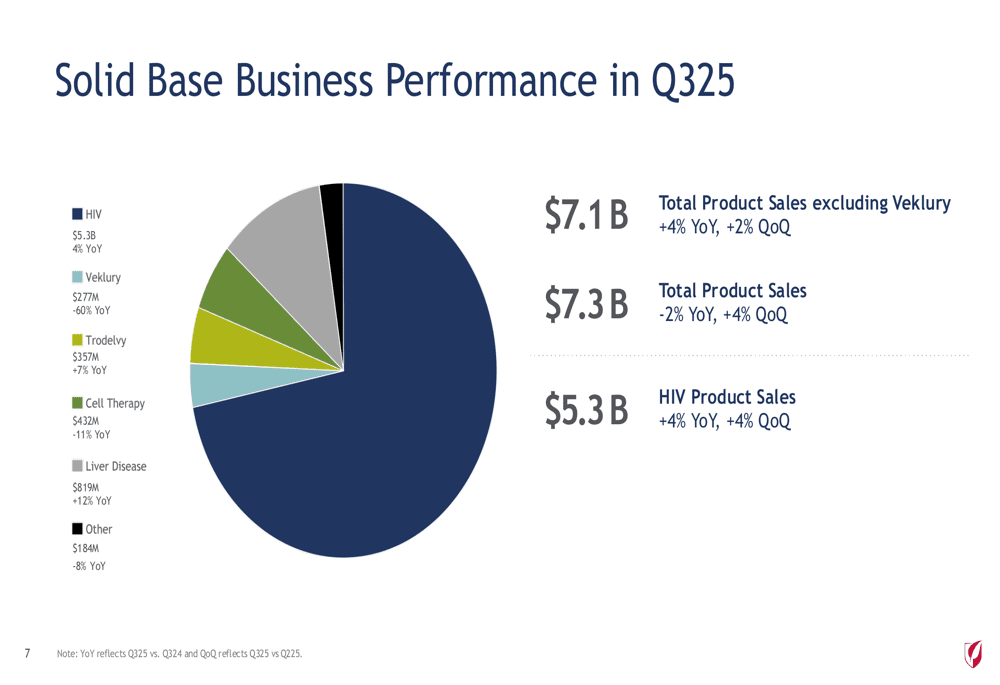

Gilead Sciences (GILD) has demonstrated considerable market resilience, with its latest Q3 2025 results showcasing a significant uplift in its full-year guidance. This strategic upward adjustment is directly attributable to the sustained strength of its HIV portfolio, a bedrock of the company’s revenue generation, and the accelerating traction of its newer product lines. This performance provides a notable contrast to broader market volatility, underscoring Gilead’s robust operational execution and its agile adaptation to evolving healthcare demands. Historical patterns in the biotechnology sector indicate that companies with strong, recurring revenue streams, such as those from established drug franchises, are inherently better positioned to navigate economic uncertainties, a trend that was similarly observed across major biopharmaceutical entities during the market turbulence of 2022. The company’s proactive approach to market challenges and its consistent delivery of results solidify its standing in a competitive landscape.

A deeper examination of Gilead’s Q3 financials reveals an impressive increase in revenue, fueled by both its established HIV treatments and its emerging therapeutic innovations. The management’s decision to raise guidance is a direct reflection of sales figures exceeding expectations and a positive outlook for market penetration of its latest offerings. The company’s unwavering commitment to research and development is demonstrably translating into tangible commercial successes, thereby fortifying its financial health. Key indicators such as improved gross margins and efficient cost management are likely contributors to this optimistic outlook, as evidenced by the projected earnings per share (EPS) growth. The current Price-to-Earnings (P/E) ratio suggests a reasonable valuation, particularly given these strong fundamentals, while robust free cash flow generation further bolsters investor confidence in the company’s overall financial stability and long-term prospects. Analysts are closely watching for continued margin expansion and R&D pipeline advancements.

In comparison to its peers within the biopharmaceutical industry, Gilead appears to be outperforming in critical growth areas, most notably within the HIV treatment segment. While competitors such as ViiV Healthcare and Merck continue to invest heavily in innovation, Gilead’s comprehensive product pipeline and entrenched market presence in HIV have afforded it a distinct competitive advantage. The company’s strategic approach to acquisitions and licensing agreements has also been instrumental in broadening its therapeutic reach and expanding its market share across various segments. While regulatory landscapes remain a constant factor, they have not substantially impeded Gilead’s progress in these vital therapeutic domains, thereby enabling sustained revenue generation and market leadership, a consistent theme observed across major biopharmaceutical entities operating within regulated markets in accordance with SEBI guidelines.

From an investor’s standpoint, Gilead’s increased guidance for 2025 presents a highly compelling case for continued investment. The company’s proven ability to consistently deliver strong financial results, particularly within its core HIV business, coupled with the promising traction of its new products, effectively mitigates perceived risk and enhances upside potential. While inherent challenges such as patent expirations and ongoing competitive pressures persist, the current performance trajectory and forward-looking guidance suggest a positive near-to-medium term outlook for the stock. Key upcoming events to monitor closely include the release of further clinical trial results and additional updates on new product launches, which are anticipated to act as significant catalysts for stock appreciation, with some analysts conservatively projecting a potential 15% upside. Investors should remain cognizant of regulatory developments and clinical trial outcomes.

Related Topics:

GILD, Gilead Sciences, Gilead Q3 2025, HIV treatment, Biotechnology sector, Pharma earnings, Guidance raise 2025, Biotech stock analysis, Healthcare industry trends, GILD stock analysis