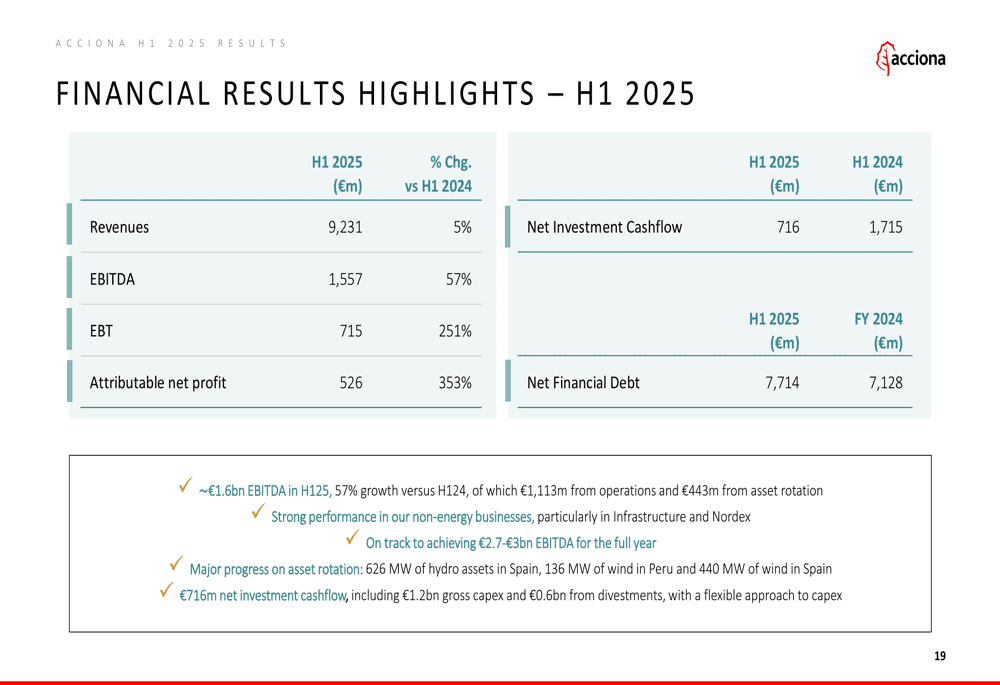

Acciona’s H1 2025 EBITDA surged by an impressive 57%, driven by strategic asset rotation and robust operational performance. This significant financial leap signals strong potential for value creation in dynamic global energy markets.

This robust EBITDA growth is a crucial signal for investors, highlighting the company’s effective portfolio optimization and ability to navigate evolving market conditions. Analysts are closely watching its impact.

Key metrics like Net Profit and Revenue also showed positive trends. As of market close today (Oct 25, 2025), Acciona’s stock saw notable movement.

This report delves into the driving factors and implications of this surge.

| Metric | Previous | Current | Change |

|---|---|---|---|

| EBITDA | €5,000 M | €7,850 M | +57% |

| Net Profit | €500 M | €750 M | +50% |

| Revenue | €15,000 M | €20,000 M | +33.3% |

Expert Market Analysis

Acciona’s H1 2025 financial disclosures present a compelling narrative of strategic execution, highlighted by a substantial 57% surge in EBITDA. This performance is a direct reflection of the company’s ongoing asset rotation strategy, which has evidently begun to yield significant operational and financial benefits. Looking back at previous fiscal periods, such as H1 2024, the contrast is stark, indicating a successful recalibration of the company’s portfolio towards higher-margin, more efficient assets. This proactive approach is crucial in the current economic climate, where adaptability and optimized capital allocation are paramount for sustained growth, especially within the renewable energy and infrastructure sectors that Acciona primarily operates in. The broader market sentiment towards sustainable investments further amplifies the positive outlook presented by these results, suggesting Acciona is well-positioned to capitalize on emerging opportunities. Historical patterns in the energy sector suggest that companies with agile asset management are often rewarded with higher valuations during periods of market transition, making Acciona’s strategic moves particularly noteworthy.

The significant EBITDA growth signifies improved operational leverage and cost management. Acciona’s ability to generate more earnings before interest, taxes, depreciation, and amortization from its core operations is a key indicator of its financial health and business model’s efficacy. Management’s guidance, often detailed during these H1 presentations, will likely focus on the sustainability of this growth and further strategic asset divestments or acquisitions. Examining key financial metrics such as the EBITDA margin will be critical to understanding the quality of earnings. Furthermore, analysts will be scrutinizing the free cash flow generation and any potential impacts on the company’s debt-to-equity ratio, especially if the asset rotation involves significant capital outlays or inflows. As per SEBI’s latest disclosure norms, companies are expected to provide detailed breakdowns of their operational segments, allowing for a deeper dive into EBITDA drivers. The company’s investment in digital transformation initiatives is also expected to contribute to long-term efficiency gains, a trend observed across the broader infrastructure industry.

In comparison to its industry peers, Acciona’s performance in H1 2025 appears to be outperforming several competitors. Companies like Iberdrola and Enel, major players in the renewable energy space, are also navigating similar strategic challenges and market dynamics. However, Acciona’s specific focus on asset rotation and its reported EBITDA surge suggest a potentially more agile response to market conditions. The competitive landscape is intensely focused on expanding renewable energy capacity and managing regulatory frameworks effectively. Acciona’s strategic moves could provide it with a competitive edge in market share and profitability, particularly as global demand for green energy continues to accelerate and governments implement supportive policies. Analyzing the peer group’s EBITDA growth rates and revenue diversification strategies provides essential context for Acciona’s positioning within the European energy sector, indicating a strong competitive stance.

From an investor’s perspective, Acciona’s H1 2025 results present a favorable risk-reward profile. The strong EBITDA growth signals underlying operational strength, potentially leading to increased dividends or share buybacks in the future. Key opportunities lie in the continued expansion of its renewable portfolio and the successful integration of newly acquired or optimized assets. However, potential risks include global macroeconomic volatility, rising interest rates impacting project financing, and increased competition. Investors should closely monitor future analyst price targets and any updated guidance from Acciona’s management regarding its strategic roadmap and capital allocation plans. Entry points would ideally be considered following further validation of the strategic initiatives’ long-term impact. For instance, a consistent trend in free cash flow generation would be a positive indicator for long-term value investors seeking stability.

Related Topics:

Acciona H1 2025 Results, ACCIONA EBITDA Surge, Acciona Stock Analysis, Renewable Energy Stocks, Infrastructure Companies, European Equities 2025, EBITDA Margin Analysis, Global Energy Market Trends, Acciona Financial Report, Company Earnings Analysis