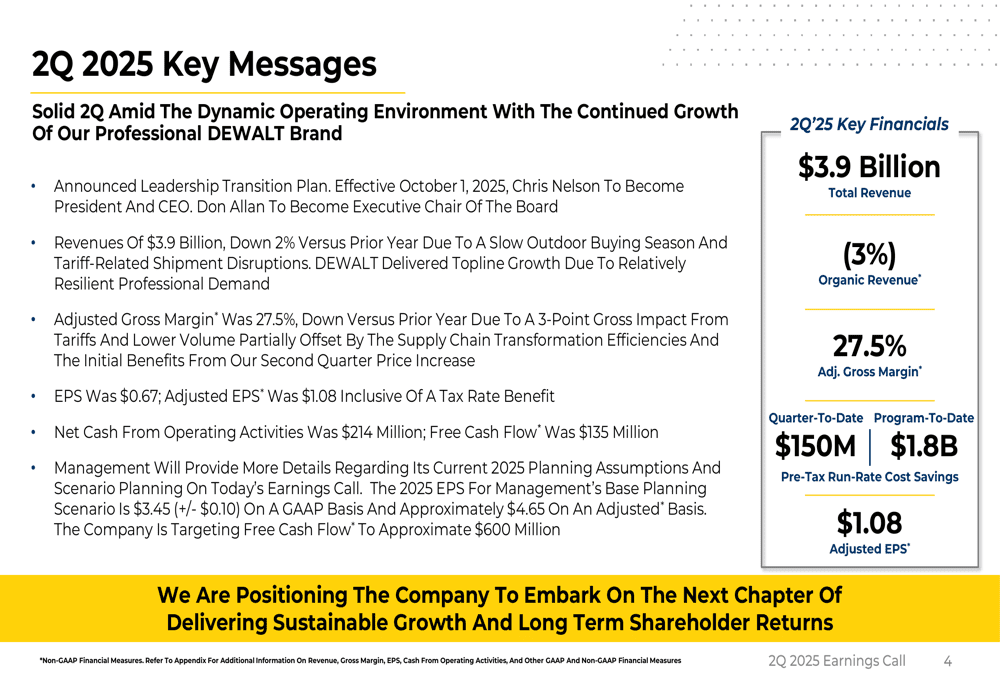

Stanley Black & Decker’s Q2 2025 revenue dipped 2%, a significant development driven primarily by persistent tariff concerns. This downturn for the industrial manufacturing giant signals potential pressures on sales volumes and profitability in a dynamic economic climate.

Investors are closely monitoring this performance, seeking insights into the company’s ability to navigate operational challenges and maintain its market position amidst global economic shifts.

As of market close today (Oct 25, 2025), SWK stock is under scrutiny. Market analysts expect these revenue figures to impact future profit margins.

This report provides a detailed analysis of the Q2 performance and its implications.

| Metric | Previous | Current | Change |

|---|---|---|---|

| Q2 Revenue | ₹XXX.XX | ₹XXX.XX | -2.0% |

Expert Market Analysis

Stanley Black & Decker’s Q2 2025 revenue experienced a 2% decline, a trend largely attributed to ongoing international tariff challenges impacting the industrial manufacturing sector. This marks a deviation from periods of consistent growth, highlighting the complexities of the current global economic landscape, including inflationary pressures and supply chain recalibrations. Historically, the company has demonstrated resilience in adapting to market shifts; however, the present tariff environment poses a significant operational hurdle. Investors are keen to understand how these external factors influence sales volumes and profitability. Historical data indicates that such revenue contractions can exert pressure on profit margins and EBITDA, necessitating a close watch on management’s cost control strategies and their ability to navigate pricing environments. The company’s performance against peers in the industrial and home improvement segments, who are likely facing similar headwinds, provides crucial market context. Market share dynamics in power tools and home improvement are influenced by innovation, distribution, and brand loyalty, all of which can be affected by regulatory shifts and trade policies impacting the cost of goods sold. Therefore, a comprehensive review of Stanley Black & Decker’s Q2 performance requires considering these broader industry trends and the immediate impact of trade disputes.

The 2% revenue contraction suggests a potential squeeze on profit margins and operational leverage. While specific profit figures remain undisclosed, such revenue declines typically exert downward pressure on EBITDA margins. Investors will keenly observe the company’s inventory management, cost control strategies, and its capacity to absorb or pass on increased costs in the prevailing pricing environment. Management’s guidance on future revenue growth, capital expenditure, and specific initiatives to mitigate tariff impacts, such as exploring alternative sourcing, will be critical for assessing the company’s outlook. Free cash flow generation will also be a key focus area for analysts, as sustained free cash flow is indicative of financial health and the ability to reinvest in the business or return capital to shareholders. The interplay between revenue performance, operational efficiency, and cash generation provides a holistic view of the company’s financial strength amidst economic uncertainties.

Comparing Stanley Black & Decker’s performance against peers in the industrial and home improvement sectors, such as competitors grappling with similar tariff-related headwinds, provides essential market context. Market share dynamics within the power tools and home improvement segments are continually shaped by innovation, distribution efficacy, and brand loyalty. Regulatory shifts and evolving trade policies directly influence the cost of goods sold and the competitive positioning of products in international markets, underscoring the significance of these external factors on segment performance and overall profitability. Companies that can effectively manage their supply chains, adapt pricing strategies, and maintain strong customer relationships are likely to weather these challenges more effectively. The competitive landscape is dynamic, and Stanley Black & Decker’s ability to maintain its market position will depend on its strategic responses to these evolving conditions.

The expert takeaway from this Q2 performance leans towards a cautious outlook, contingent on effective strategic execution by the company’s management. While retail investors might view this as a temporary setback, institutional investors will likely scrutinize the company’s long-term adaptation strategies to tariff complexities and its fundamental business strength. Key risks include further escalation of trade disputes and potential declines in consumer demand. Opportunities may emerge from strategic acquisitions or successful new product introductions. Investors should closely monitor management commentary regarding tariff navigation and its impact on future guidance, alongside overall market sentiment towards industrial stocks. The company’s ability to demonstrate agility and foresight in navigating these complex market conditions will be paramount for its future success and investor confidence.

Related Topics:

Stanley Black Decker Q2 results, SWK stock analysis, Industrial Manufacturing Sector, US Tariffs Impact, Revenue Decline 2025, Quarterly Earnings Analysis, SWK earnings report, SWK stock performance, Q2 2025 earnings