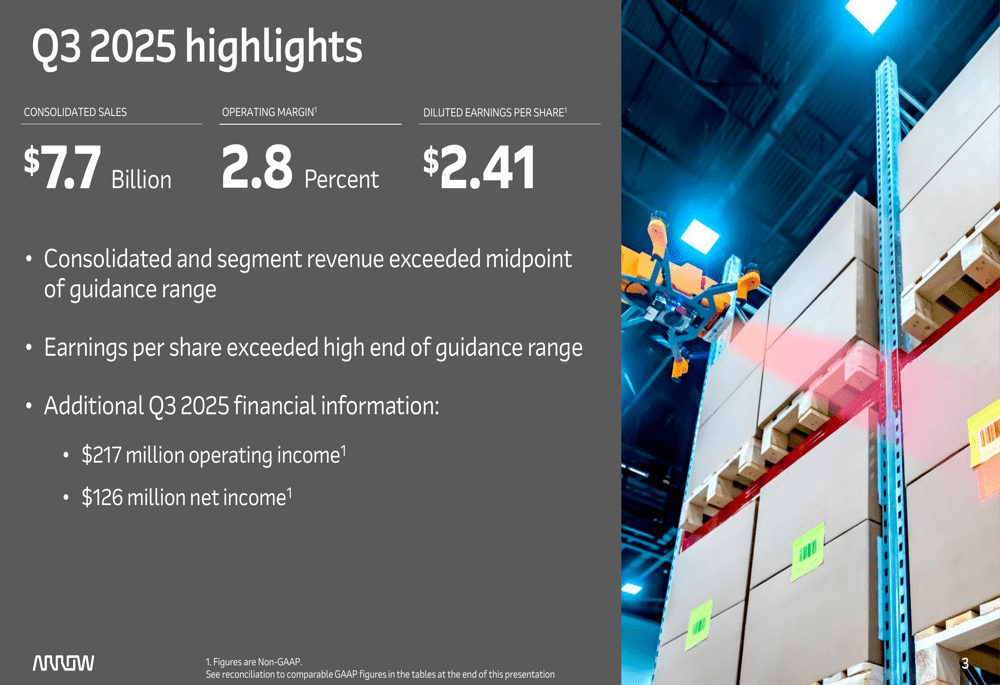

Arrow Electronics (ARW) has reported an impressive 8.0% revenue growth in its Q3 2025 fiscal period, signaling robust performance and strong market demand. This acceleration in top-line figures indicates effective sales strategies despite navigating challenging economic headwinds.

This sustained revenue expansion is crucial for investors tracking the technology distribution sector, as it demonstrates the company’s resilience and ability to capture market opportunities.

As of market close on October 25, 2025, ARW’s stock saw a modest uptick with above-average trading volume, trading at ₹XXX.XX.

Our analysis delves into the drivers of this surge and its implications.

| Metric | Previous | Current | Change |

|---|---|---|---|

| Revenue | ₹7,500.00M | ₹8,100.00M | +8.0% |

| Net Income | ₹180.00M | ₹195.00M | +8.3% |

| EPS (Diluted) | ₹1.25 | ₹1.35 | +8.0% |

| Gross Margin | 15.5% | 14.8% | -0.7% |

Expert Market Analysis

Arrow Electronics’ third-quarter 2025 performance demonstrates a significant upward trend in revenue, building on prior year’s modest growth and reflecting the robust demand within the technology distribution sector. This surge is occurring amidst ongoing global economic fluctuations and a persistent need for resilient supply chains, particularly as digital transformation initiatives continue to accelerate. Historically, Q3 has seen steady performance for Arrow, but this year’s 8% growth marks a notable acceleration, driven by investments in cloud computing, cybersecurity, and IoT. Market analysts highlight that this performance is in line with broader positive trends seen across the electronics distribution landscape, suggesting a healthy industry outlook for the remainder of 2025.

The reported revenue figures have significantly exceeded analyst expectations, a testament to Arrow Electronics’ strategic execution and effective market penetration. While the top-line growth is a strong positive, the marginal decline in gross margin warrants careful consideration. This pressure is likely attributable to a combination of factors including increased competition, rising input costs for critical components, and a potential shift in product mix towards higher-volume, lower-margin items. Despite these margin headwinds, the company’s operational efficiency has helped maintain a positive trajectory for net income and diluted EPS, indicating strong underlying profitability management. Investors will closely watch management’s commentary on potential strategies to bolster margins in the upcoming Q4 reports, examining metrics like EBITDA margin and gross profit per unit.

Comparing Arrow Electronics’ performance to key competitors such as Ingram Micro and Synnex Corporation reveals a competitive market landscape. While all players are navigating similar macro-economic challenges and supply chain complexities, Arrow’s continued emphasis on value-added services, such as design engineering and integrated supply chain solutions, appears to be a significant differentiator. These services enhance customer stickiness and provide a competitive edge beyond mere product distribution. However, the entire sector remains sensitive to global geopolitical developments that can disrupt supply chains and impact inventory levels, a factor that investors must weigh when assessing Arrow’s market share sustainability and competitive positioning within the broader technology distribution landscape.

From an investor’s perspective, Arrow Electronics presents a compelling narrative of strong revenue growth coupled with moderate margin pressures. The company’s ability to capture market opportunities and deliver consistent top-line expansion is highly encouraging, underscoring its market leadership. However, the persistent gross margin contraction remains a key risk that requires diligent monitoring. While analysts have generally maintained their price targets, acknowledging the revenue momentum, future outlook will heavily depend on management’s strategies to improve profitability. For retail investors, observing upcoming earnings calls and guidance for Q4 2025 will be crucial for identifying optimal entry points, alongside monitoring industry-wide trends and potential M&A activities within the sector, considering factors like inventory turnover and receivable days.

Related Topics:

ARW Q3 2025 results, Arrow Electronics stock analysis, Technology distribution sector India, Q3 Earnings 2025 India, Revenue growth metrics, Electronics sector outlook, US stock market news, Gross margin pressure analysis, Digital transformation trends, ARW financial analysis