Key Takeaways

Explore joint accounts for financial unity in 2025. Expert analysis on fostering shared goals and overcoming financial separation. Insights for couples managing personal finance.

Market Introduction

Explore joint accounts for financial unity in 2025. Expert analysis reveals how shared financial goals can be fostered, offering insights for couples navigating personal finance. This article delves into the dynamics of money management for married individuals. As of market close November 11, 2025, understanding these dynamics is crucial for investors.

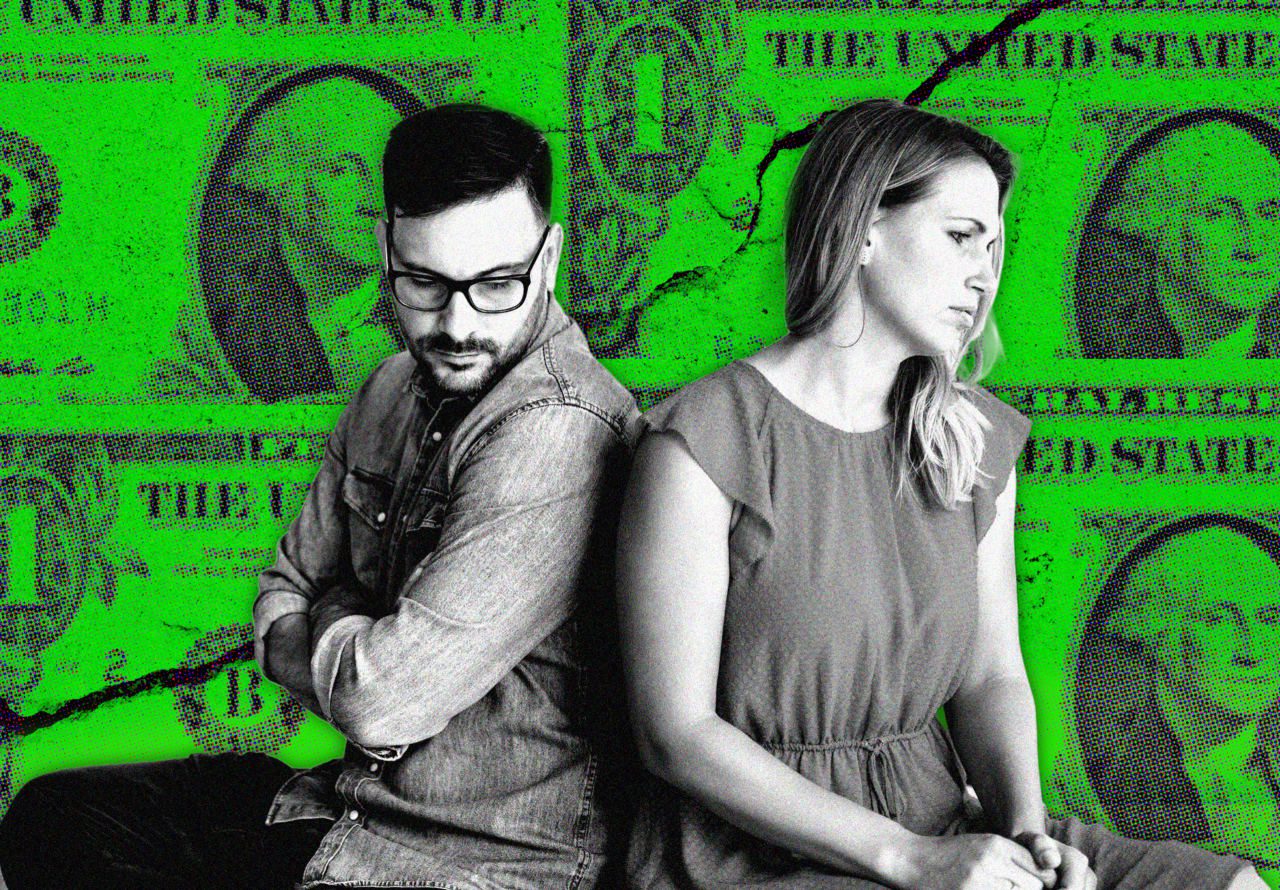

Separating finances for over a decade is unusual and can impact shared goals. While joint accounts address bill payments, effective communication remains the core challenge, mirroring corporate strategies for efficiency and trust.

Divergence in financial management can affect wealth accumulation due to differing investment philosophies. This divergence necessitates a proactive approach to financial integration. We explore implications and solutions for couples.

The article provides a deep dive into the synergy of shared finances and wealth building.

In-Depth Analysis

Historical financial patterns indicate that couples aligning their strategies achieve shared goals more effectively than those with divergent approaches. While individual autonomy is valued, a prolonged lack of a shared financial vision can significantly strain long-term objectives such as retirement planning and significant asset acquisition, like property. From an investor’s perspective, this divergence in risk appetites and planning horizons, often seen in couples maintaining separate finances for over a decade, can hinder overall wealth accumulation and synergy. This situation prompts crucial questions about marital financial synergy and the necessity of proactive planning, especially concerning major life events. Broader market trends for 2025 suggest an increased emphasis on financial consolidation across various asset classes, impacting personal finance strategies and the utility of joint accounts.

From a financial management standpoint, the absence of a joint account can lead to considerable inefficiencies in managing household expenses and investments. Key financial metrics such as consolidated savings growth, synchronized investment portfolios, and simplified tax filing become more challenging to attain. While individual financial discipline is commendable, non-unified investment strategies may result in missed opportunities in wealth creation, such as leveraging joint investment schemes or optimizing tax benefits. Macroeconomically, consumer spending is significantly influenced by household financial confidence, which is often bolstered by a unified financial front. The psychological aspect of financial partnership, strengthened by shared oversight, aligns with expert advice emphasizing open communication as a cornerstone of marital success. Key indicators like the Household Financial Confidence Index will be crucial for monitoring this trend.

Comparing personal finance scenarios to corporate partnerships reveals striking parallels that inform our outlook. Companies with strict departmental financial silos often struggle with strategic alignment and resource optimization, mirroring couples with separate finances. For instance, industry giants like Infosys and Tata Consultancy Services (TCS) emphasize integrated financial reporting and shared Profit & Loss (P&L) responsibility to drive collective performance. This is particularly evident in the IT sector, where collaborative project funding and unified R&D investments are key drivers of success. Regulatory frameworks, such as those established by SEBI, promote transparency and accountability—principles that can guide personal financial relationships toward greater trust and shared success, influencing broader market dynamics and investor sentiment positively.

The expert takeaway is that while personal financial separation is a valid choice, it demands robust and continuous communication to prevent misunderstandings and misalignment. For couples considering a joint account, it presents a significant opportunity to redefine their financial partnership, fostering enhanced collaboration and a stronger sense of shared purpose. The risks of continued separation include potential resentment, missed financial opportunities, and a lack of cohesive long-term planning. Thoughtful financial integration can foster greater economic security and a more cohesive partnership. Key events to monitor include how couples navigate future financial decisions, particularly large-scale ones like property purchase or retirement planning, which will shape personal finance trends for 2025.